In last post I questioned some of the Swedish government’s fascination with Turkey’s recent democratic reforms, which although carry the label of democratic reforms, do not address the fundamental problems. This post is about the government’s infatuation with the Turkey’s economic success.

In addition to last year’s Turkish state visits to Sweden (see here and here), a number of more focused trade-relation visits have occurred (see here, for an example). It was likely no coincidence that, sitting in Stockholm University Aula Magna during the inauguration ceremony for the new Swedish institute for Turkish studies (SUITS) last year, that the ratio of businessmen-to- academics seemed rather high.

One can understand the lure of Turkey’s economy for Swedish firms – the country has 74 million inhabitants, a relatively young population, is the 17th largest country in terms of IMF-measured PPP GDP. Moreover, the government’s expansion in infrastructure and technology sectors coupled with a burgeoning middle class, the possibility of a resolution to the decades-long conflict in the east, as well as a possible stepping stone into the Middle East, all add to the pull.

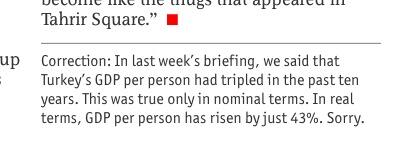

A ubiquitous talking-point in Turkish foreign policy is the claim that, under AKP rule, the country’s GDP has tripled. This, however, is a misleading number as it relies on valuing US dollars of Turkey’s GDP at current prices, thus pooling both inflation of the dollar and the real appreciation of the Turkish lira on top of real growth. In real terms, Turkish GDP at constant prices grew by 64 percent between 2002-2012, and GDP per capita grew by 43 percent. A decent growth rate, but nowhere near the miraculous.

This number has nonetheless made its mark, and hilariously seeped into one of The Economist’s articles on Turkey’s economy, resulting in a correction that will make nerdy economists giggle for centuries.

A discussion of this hilarity took a surreal turn when Turkey’s finance minister, Mehmet Simsek, weighed in and, in front of one of the leading international economists in this world, saw his credentials as an economist… well, somewhat perturbed.

The incident was not without comical appeal, the least since Turkey still has inflation rates in the order of 7-8 percent, and only ten years ago experienced rates above 20 percent. (For more, see Emre Deliveli and Dani Rodrik’s posts on this event).

Somewhat less fun has been to see how this widespread misleading figure of a country’s economic performance has taken root in the Swedish government’s (as well as other governments’) push to promote economic relations with Turkey.

In my last post I noted a rather unfortunate op-ed in a Swedish daily, published in November last year by Sweden’s foreign minister just before Erdogan’s state visit to Sweden. In addition to the rather provocative title, “Erdogan’s Turkey is on the right path”, the article also adopted the misleading talking point in praise of recent growth in current prices.

Erdogan will be accompanied by five ministers and a business delegation of almost 200 people. This is a sign of increasingly important trade relations. Since the new millennium began, Turkey has become integrated into the global economy in earnest. Its GDP has trebled over the past decade. This has been the result of liberal reform policies and the customs union with the EU that was created in 1995.

This is unfortunately not an isolated incident – earlier the same year, in association with another state visit (this time by President Abdullah Gul) a post appeared on the Swedish Foreign Ministry’s website with the same claim (here). It also features on the website of the Swedish Consulate in Istanbul (here), the main state-owned trade and Investment council and the go-to link for those googling “Sweden trade Turkey”. Not surprisingly, this figure then also makes its way into news articles (see here, here, and here)

So what? After all, this is the Foreign Ministry, not the Finance Ministry. The issue, however, is that misleading numbers of Turkey’s performance have come in association with a significant push to greater Swedish exposure to the Turkish economy. Again, from the Swedish Foreign Ministry’s press releases at the time of President Gül’s state visit:

Turkey is one of the most dynamic growth markets today, and has succeeded in opening up its industrial sector, exposing it to competition and promoting diversification. The country has tripled its GDP per capita in ten years and has acquired a growing middle class. The main challenges now lie in attracting more investment and raising the educational level.

Ok, so growth? check! Middle class? Check! Liberal economic policies? Check! Well, not so fast.

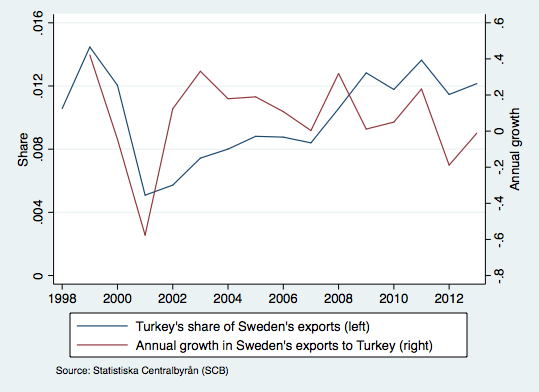

If Turkey is such a dynamic growth market for Sweden, then we should have observed an unprecedented expansion of exports to Turkey of high-value goods that middle classy people like to consume. Unfortunately, neither of these are necessarily true. First of all, as the below graph shows, Swedish exports to Turkey were if anything higher before its financial crisis in 2001. The years after this severe crisis, exports to Turkey were understandably unusually low. Secondly, the growth in exports to Turkey have been stagnating in the last couple of years. (I’m going to let it slide that the Swedish Consulate in Istanbul chose to publish on their website only the 2011 growth value).

Thirdly, the composition in exports to Turkey has shifted downwards in the value chain. Via the Observatory of Economic Complexity at MIT, I compared the type of goods exported in 1999 and in 2011. Here’s 1999:

And here’s the same for 2011:

As clear from the these two graphs, the largest relative increases have been in metal ores, at the expense of telecom equipment (read: Ericsson). So much for Swedish high-tech goods gobbled up by citizens of “The New Turkey”. (By the way, congratulations, LKAB!)

Whereas Turkey has claimed back its previous position as a significant trade partner to Sweden, increases in Swedish foreign direct investments (FDI) in Turkey have remained much more muted. Despite several cases where Swedish firms have bought assets in Turkey, in 2013, Turkey still only ranked 40th largest recipient of Swedish FDI, behind many other emerging economies (again, according to SCB).

So why have we not seen more Swedish investment in Turkey if it is such a booming economy?

One pretty obvious reason is the country’s institutions. In contrast to the Swedish trade relations organizations, its American counterpart is quick to note this (here) as a major challenge to doing business in Turkey:

U.S. exporters face many of the same challenges that exist in other semi-developed countries, such as contradictory policies, regulations and documentation requirements, lack of transparency in tenders and other procurement decisions, and a time consuming, unpredictable judiciary and legal and regulatory framework. Careful planning and patience are the keys to success in Turkey.

A possible reason why this obvious issue does not appear in any of the government’s published material (that I could find on their websites), is that the government hopes to be able to leverage its exceptionally good diplomatic relations with Turkey (again, from the ministry’s website here):

“The country is quite centrally controlled and Swedish companies often need official support to succeed. In this way, good diplomatic relations with Turkey can make a difference and make life easier for the business sector.

The idea that good diplomatic relations will substitute for good institutions for investment is a rather strong assumption. Especially since recent Turkish history is full of cases of state intervention in private firms. In recent years, investors have gotten much experience in this.

1. In 2009, Doğan Holding was awarded a tax fine of $2.5bn, roughly four fifths of its market value at the time. Several news outlets owned by Doğan had previously published articles suggesting the ruling AKP was bent on leading Turkey towards religious rule, and these had then been used as evidence in a court case to ban AKP (which, in the end, the court didn’t do). Several other media companies have also gone into receivership after fraud charges. (See this Economist article from the time.)

2. During the Gezi protests last year, a hotel owned by the Turkish conglomerate Koç Holding allowed protesters shelter from a brutal police crackdown. About a month later, the government began tax audits into three Koç-owned companies. The conglomerate, one of the largest in Turkey, reportedly lost $1bn in stock market losses in one day (see here).

3. Earlier this year, several government-owned (or related) companies, appeared to coordinate ceasing all business relations with Bank Asya, a bank affiliated with the powerful Gulen movement. An article by Bloomberg noted these attacks on Bank Asya as a casualty in the political conflict with the Erdogan government and the Gulen movement. Between mid-Dec and early February, the company’s stock lost nearly half of its value.

4. All of these incidents have involved Turkish companies, but there have also been incidents involving Swedish companies. A case in point is the travails of Telia Sonera and its attempt to buy Turkey’s largest telecoms operator, Turkcell (see the many well-written articles by FT journalist Daniel Dombey). In 2005, a deal was reached with Cukurova Holding to purchase a majority-stake in Turkcell, but as the deal went sour, it turned into a legal battle involving TeliaSonera, Cukurova, and another Russian-owned holding company. The case dragged on for years through arbitration courts. Last year, the Turkish government ran out of patience and legislated a takeover of Turkcell’s board of directors. Using a new law that allows the government to take over boards that fail to appoint directors in line with other Turkish legislation, Turkcell thus ended up with a board made up of former AKP members. In August, two additional directors were appointed – both Swedes. A delicate situation has thus evolved, where Telia Sonera’s huge investment in Turkcell is subject o the whims of Turkey’s government, and in the future it will likely have to rely on the Swedish government’s relations with Erdogan. Further complicating the matter is that Turkcell has played a crucial role in the state security push to detain and prosecute numerous human rights and union activists, as reported by Swedish newspaper Arbetet (among several).

These are just examples of how the state can use its power to crack down on companies, when they or actors related to them, criticize the government. The journalist Kadri Gursel, in an article on the Koç audit, recently wrote

The situation is all about how domestic and foreign investments in Turkey are not under the protection of the legal system and how vulnerable they are to arbitrary and punitive covert operations by political authorities.

More subtle indications of where Turkey is heading for potential investors, are the frequent outspoken concerns from leading Turkish business associations. Ümit Boyner, former head of Turkey’s largest business association, TÜSIAD, was recently quoted in the Financial Times lamenting the political involvement of economic institutions such as the competition board, the central bank, and the banking regulator. More recent expressed concerns by its current chairman Muharrem Yilmaz (see here), has been met by accusations of treason by Erdogan. And then there’s this, via Bloomberg:

At a meeting of the European Venture Capitalist Association in Istanbul today, Turkey’s Finance Minister Mehmet Simsek got a zinger of a question: “Is it time to call the doctor?” asked Jochen Wermuth, chief investment officer at Wermuth Asset Management. Wermuth was referring to the notion being promoted by Prime Minister Recep Tayyip Erdogan and his government that bizarre international conspiracy provoked recent protests in Turkey. He cited one particularly odd claim, from a pro-government Turkish commentator, who said the German airline Lufthansa was in on the plot because it wanted to prevent construction of a huge third airport for Istanbul and so avoid competition for its hub in Frankfurt.

Many of these firms used to have good relations with the Turkish government. Their experience is a warning sign that good relations today do not necessarily imply good relations tomorrow. And when that happens… well, let’s hope it doesn’t.

There are several reasons why Swedish firms should be interested in doing business in Turkey. There are at least as many reasons why such activities should receive well-informed, prudent advice from government agencies, and not just in backdoor meetings but on publicly available websites.

Turkey’s flawed institutions hampers its capacity to become the economic powerhouse that the government claims it has become, which it hasn’t yet, but nonetheless still could. This also limits gains of trade between Swedish and Turkish firms. The Swedish government can be a better friend to Turkey and its people by putting an end to repeating the Turkish governments talking points and shifting to an institutional focus on Turkey and its need for democratic reform. A Turkey with more open and democratic institutions will benefit firms and people alike, and not just those with the good connections to the government.

Pingback: New op-ed on what’s wrong with Sweden’s approach to Turkey | Erik Meyersson