Disclaimer: The views herein are strictly my own. I am grateful for comments from and discussions with a number of current and former EBRD employees.

[Updated as of Dec 3, 2020. Now includes comparisons with EIB investments and human rights outcomes. Since the publishing of this blog post, there has also been some threatening emails from EBRD on a related topic.]

The EBRD – a democracy-committed regional development bank

The European Bank of Reconstruction and Development (EBRD) is not just like any other development bank. Its heritage comes from the period of transition of the former Eastern bloc away from authoritarian political- and planned economic systems to democratic and market capitalist ones. Whereas there are several regional development banks who work to promote economic prosperity, the EBRD from its conception has had a political character. This is best manifested in Article 1 of its statues, which states that the Bank “may only carry out its purpose in those of its recipient member countries (countries of operations) which are “committed to and applying the principles of multiparty democracy, pluralism and market economics.”” The EBRD further specifies 14 specific criteria to make a “detailed political assessment” of what constitutes such a commitment.

Article 1, as it is written, leaves little room for exceptions to the commitment to democracy and the specification of what constitutes such a commitment correlates well with generally acceptable principles of it. The statues also do not leave room for interpretation that any of the EBRD’s other goals, such as its environmental focus, should ever take precedent over its commitment to democracy. This means that the degree to which the EBRD abides by this commitment can be easily deduced from observing standard measures of democracy.

The EBRD documents further stresses its ability to “respond flexibly to important shifts in the political situation” so that the Bank “is able to respond in an agile fashion to changing circumstances in its recipient member countries and so deliver “more for more,” or conversely, “less for less”, demonstrating a firm commitment to its political mandate and maximizing its impact and leverage.” Thus, it ought to follow that the EBRD then also do adapt to changing political circumstances.

In reality, however, the EBRD is active in authoritarian governments. It operates in Egypt as well as Central Asian countries like Kazakhstan, Turkmenistan, and Uzbekistan, where it claims to be the largest institutional investor. It also remains highly active in more recent autocracies like Turkey, as well as countries with rapidly deteriorating political institutions like Hungary and Poland.

This post serves several purposes. One is to measure the degree of EBRD investments in autocracies, and discuss some of the problems associated with this, even in the cases where the bank works with the private sector. Another is the unfortunate timing of a 2013 Transition report which seems to have suggested investing in autocracies could be advisable – at the same time that the EBRD started signing deals in autocracies. The report attributed these arguments to “modernization theory”, a controversial development view that during the Cold War was used as an excuse to support repressive right-wing dictatorships. I don’t know what made the EBRD choose to shift its business strategy, roughly around around 2013 according to the data, but I speculate around whether this may have been as a means of survival, as well as a geopolitical shift and the need to compete with other major powers as a more global development bank to facilitate the EU’s interests. The final purpose is to stimulate a debate on the purpose of the EBRD as the concept of transition seems to be changing, and to link this to the wider discussions being had within the EU over how to structure its future development bank.

The EBRD finances not just autocratic countries but also its governments

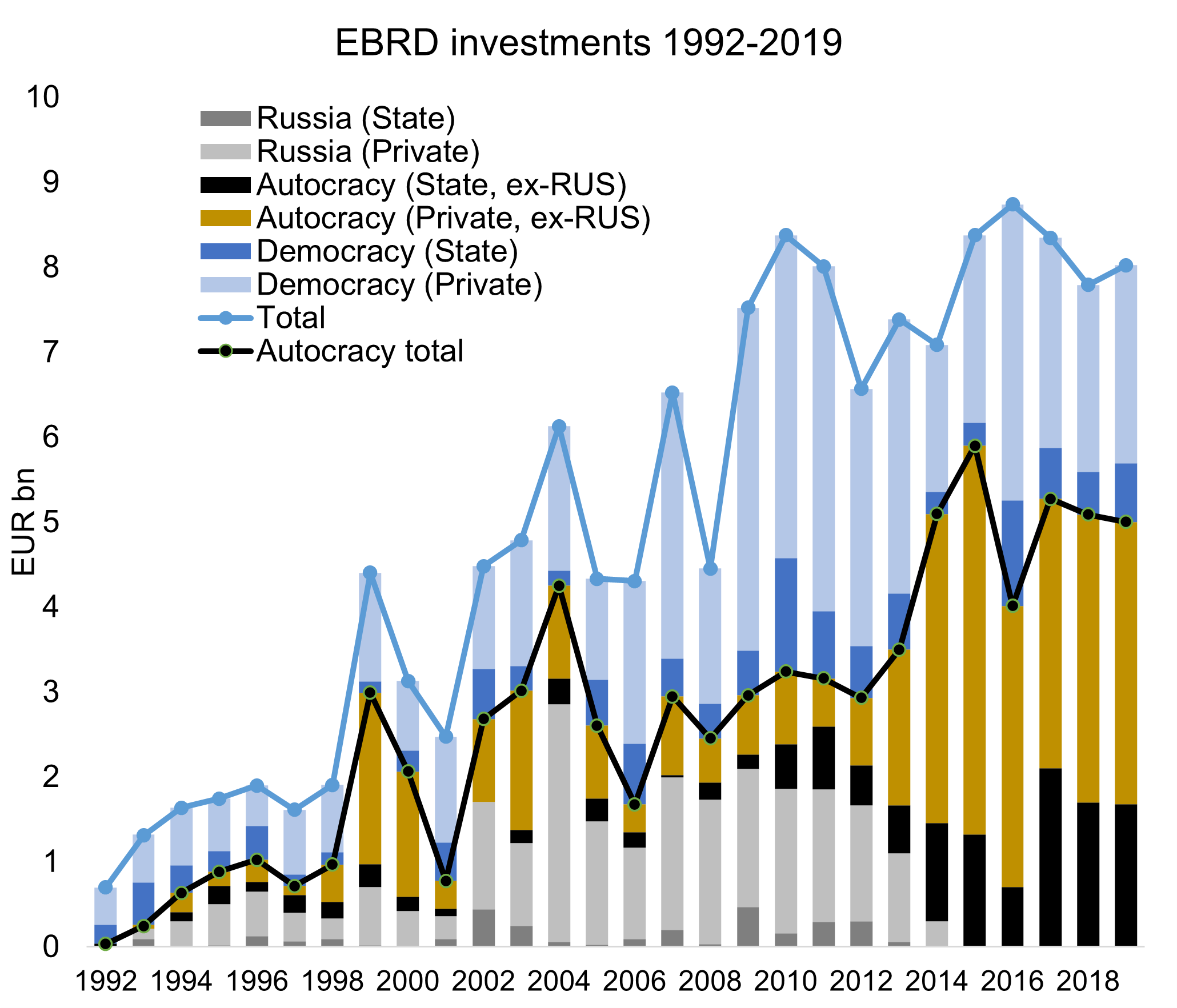

The degree to which the EBRD invests in autocratic countries can be gleaned from matching EBRD investments with the V-Dem dataset, specifically its regime classification, which assigns countries to one of four types of governments (which run from least to most democratic): Closed autocracies, electoral autocracies, electoral democracies, and liberal democracies. The graphs show investments by year of original signing, which is how EBRD publishes its projects list on its website. EBRD also assigns its investment to either the private or the government sector, which I’ve interpreted as including any of either central, state, or local governments.

Especially since 2013, the euro value of EBRD investments in autocratic countries have risen much faster than those in democratic countries, as shown below using the regime classification of Varieties of Democracy. This is despite investments in Russia declining rapidly since 2009 to the point where they cease after 2014 and sanctions make the country largely impossible to invest in. Among the democratic sample is also Czech Republic where the EBRD ceased activities in 2008 (and remains the only country to have “graduated” from the EBRD).

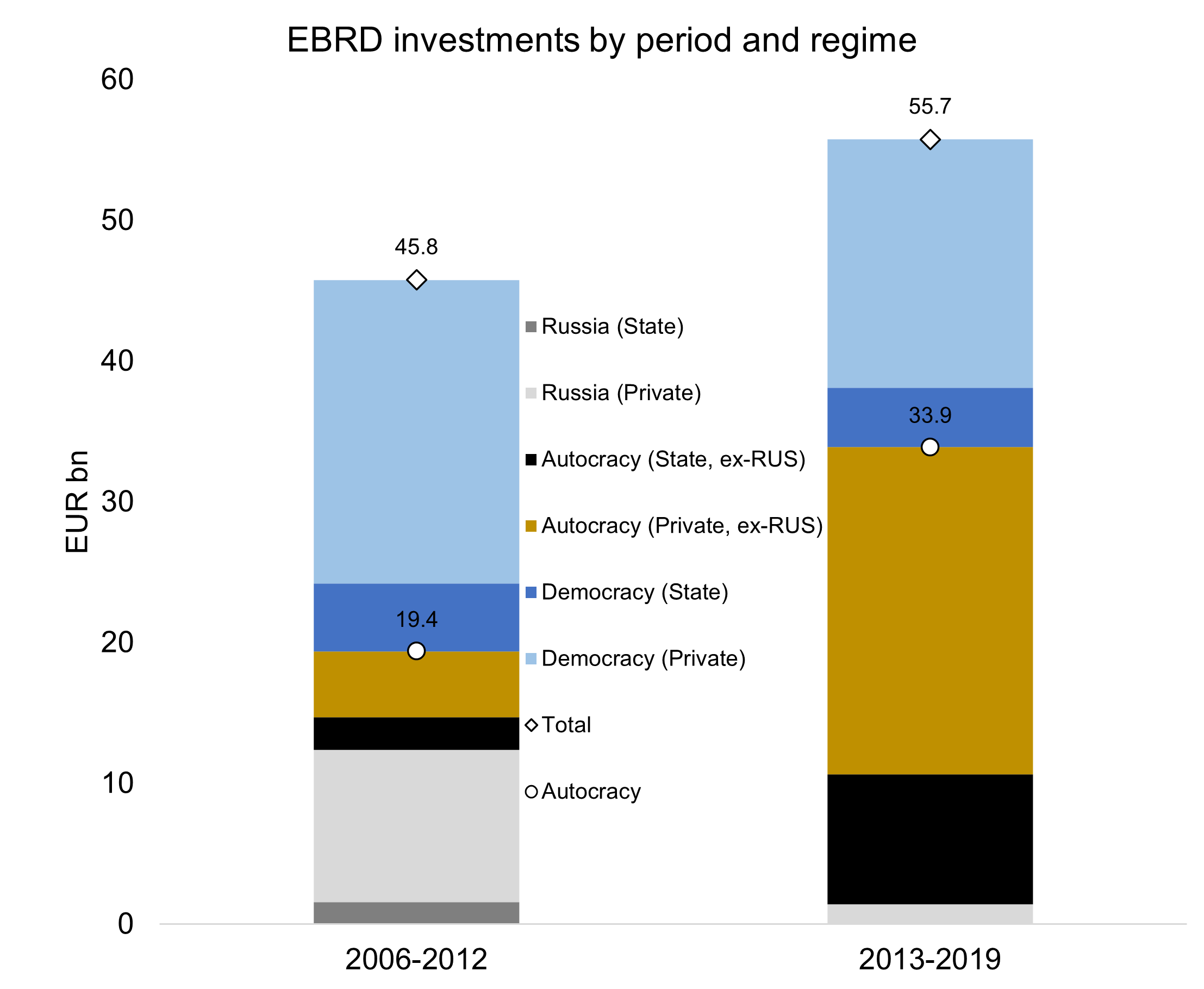

Two thirds of all investments went to autocratic countries in 2019, and a fifth went to autocratic governments. If we instead group the data by two equally large time periods, 2006-2012 and 2013-2019, we see further the degree to which the EBRD is financing autocratic countries:

- 2006-2012: In this period, around 42% of all investments went to autocratic countries, overwhelmingly dominated by Russia which by itself accounted for a fourth of all investments. Meanwhile, only about 8% went to autocratic governments.

- 2013-2019: In the last seven years, the amount flowing to autocracies has increased significantly (and more than tripled excluding Russia) and now corresponds to 60% of all investments (€33.9bn) and 17% went to autocratic governments (€9.23n). This large increase in total investments to autocratic countries (and their governments) is even more noteworthy since by 2015, Russian investments have essentially gone to zero. Although Poland sees significant deterioration in their political institutions, V-Dem continues to classify it as an electoral (although not liberal) democracy. Hungary and Turkey, however, are reclassified by V-Dem as autocracies in 2018 and 2014 respectively.

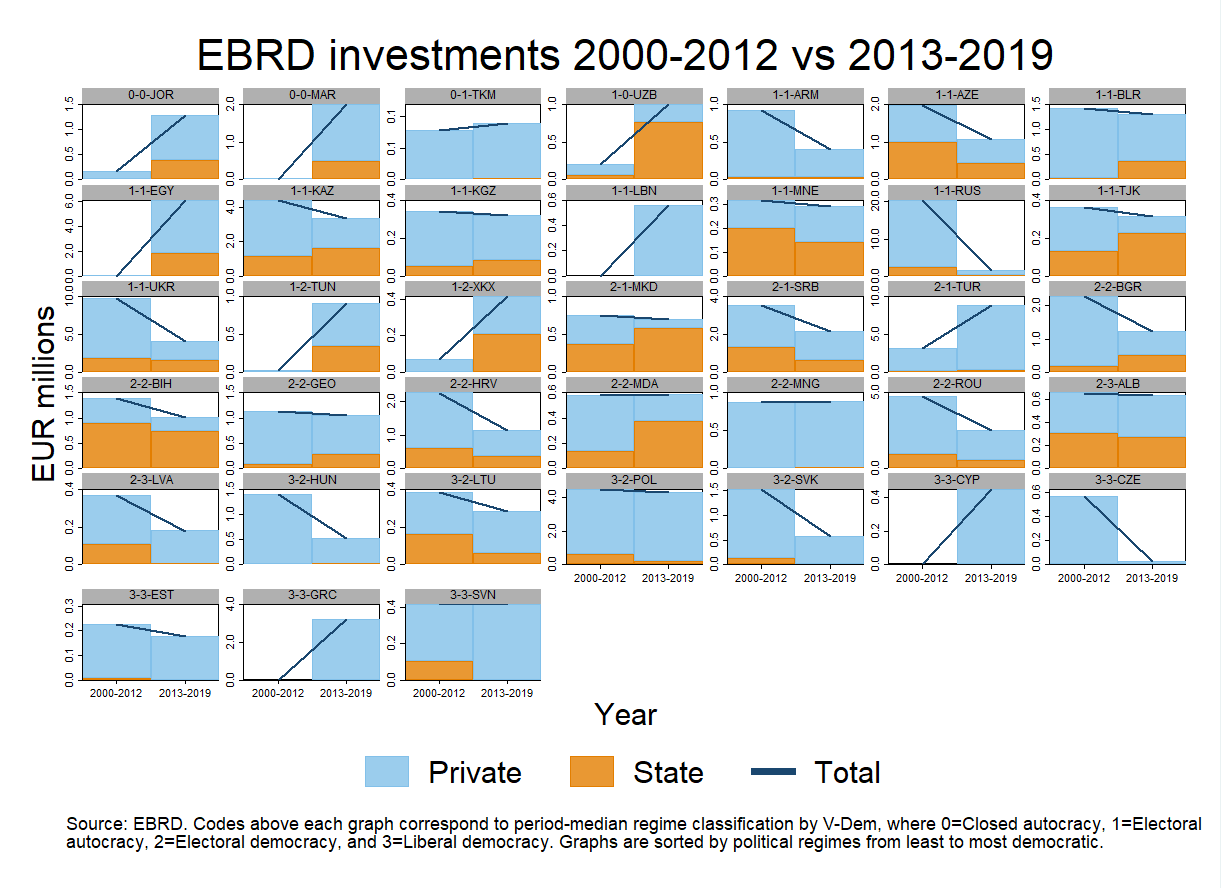

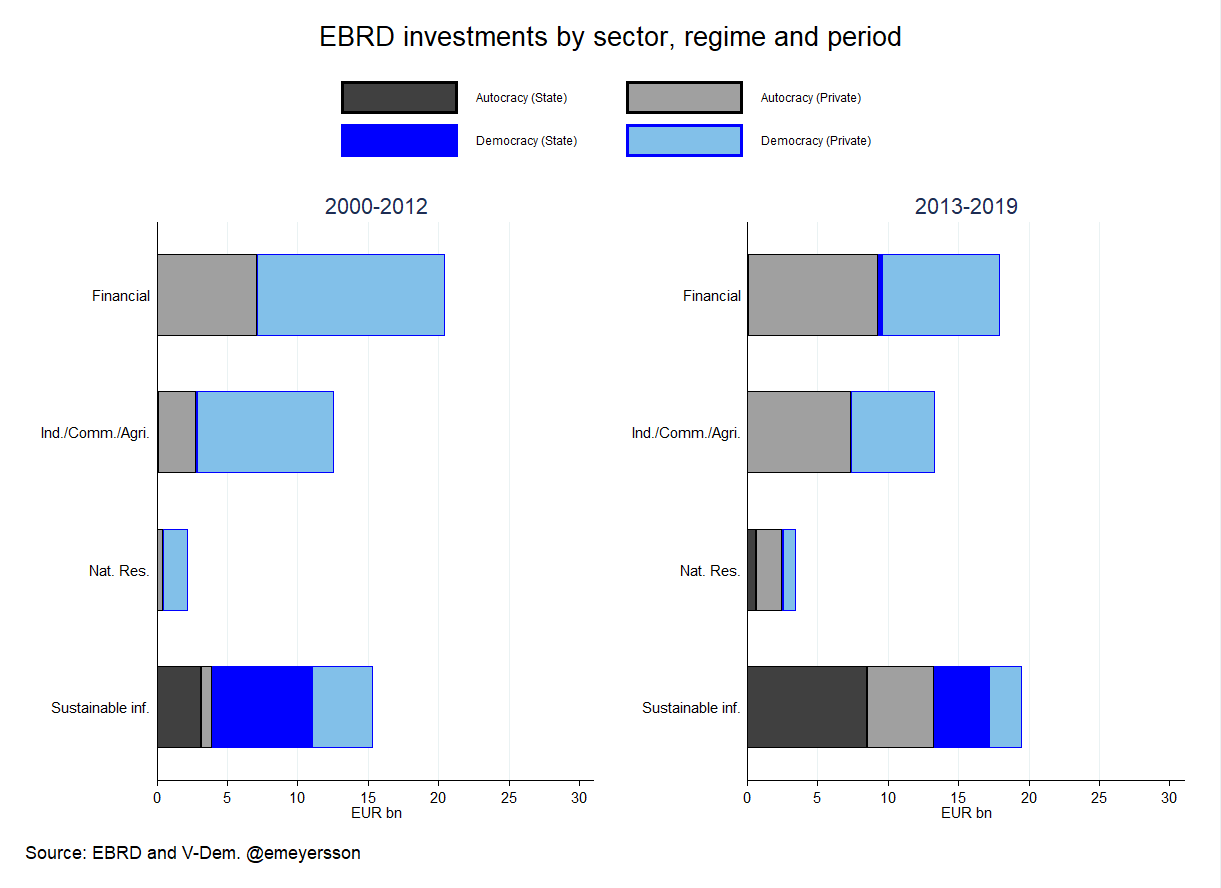

This is a dramatic increase in funds to autocracies since 2013 and serves to show that the EBRD not only finances autocratic countries, but also to a large extent autocratic governments. If we group the data by the same time periods, but by country and sector (state vs private) and sort it by political regime, we can see that even though the EBRD finances governments across both autocracies and democracies, the investment increases tends to be mostly in terms of autocratic, rather than democratic, countries (and governments).

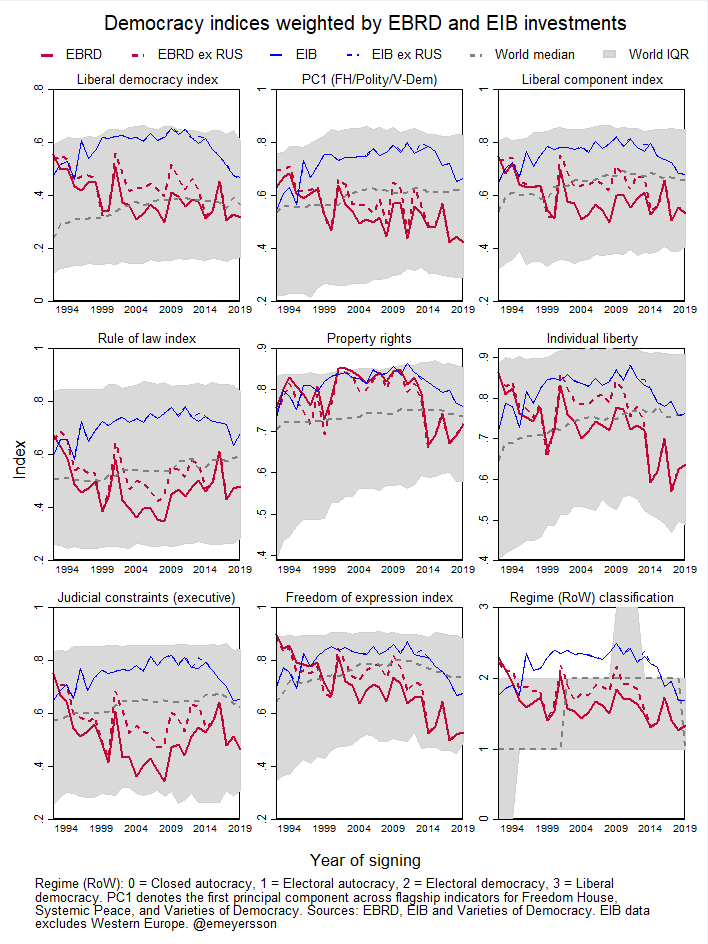

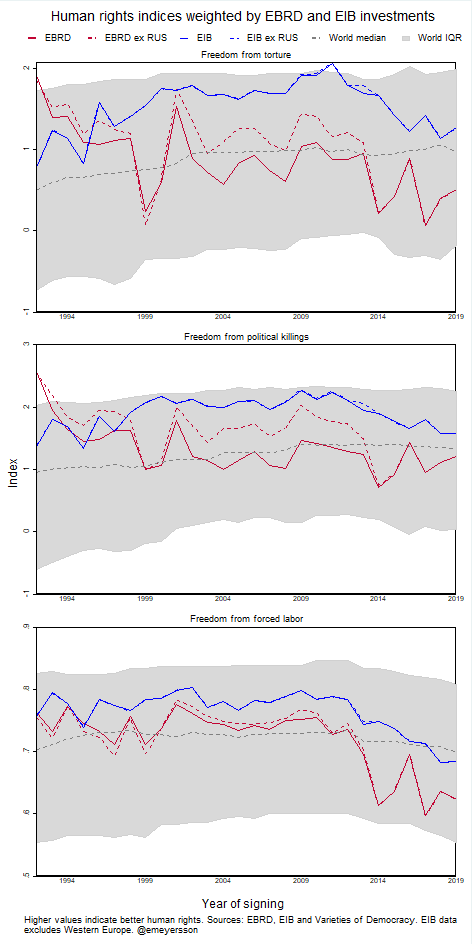

Another way to visualize the data is to weight democracy indices by EBRD investments and comparing this “EBRD universe” to the world median and interquartile range (the 25th and 75th percentiles of the distribution). I continue to focus on data from V-Dem, but for the sake of inclusion, I also construct the first principal component of indices from three common sources: V-Dem’s Liberal Democracy Index, the average of Freedom House’s Civil and Political Liberties indices, and the Polity IV index (upper middle panel). Since Russia disappears from the sample in 2014, I also plot one line with and without the country in the EBRD sample. And finally, I’ve also added the corresponding EIB-weighted index for the subsample of EIB destinations outside of Western Europe (effectively limited these countries to developing and emerging countries). The comparison is relevant as they are both Europe-centric institutions, and both considered in competition for a future role as the EU’s development bank.

Across all the above indices, the declining trend is clear and visible for the EBRD-weighted index, mostly since 2013 but in some cases earlier. As can be seen above, including Russia (solid red lines) will distort the trend somewhat, as the EBRD starts to wind down its Russia investments in the beginning of the 2010s and ceases operations by 2015. But this decline is arguably driven by the threat of sanctions, deteriorating US-Russian relations, and to some extent outside of the EBRD’s control. Instead, the red dashed lines which excludes Russia shows a clearer picture of the adverse institutional trajectory of EBRD universe of countries.

The indices of liberalism and freedom of expression (arguably close to the EBRD’s sense of “pluralism” in Article 1) are especially troubling. In the latter, the EBRD universe has fallen so far it now it is now close to the 25th percentile of the distribution. The shift in 2013 toward financing autocracies also resulted in an unsurprising plunge in economic institutions as measured by property rights. What is noteworthy, however, is that there is little evidence of improvement in the past seven years of EBRD involvement. The last graph in the lower right-hand corner is the EBRD-weighted regime, and whereas up until roughly 2010 it could be considered an electoral democracy, today it is much closer to an electoral autocracy.

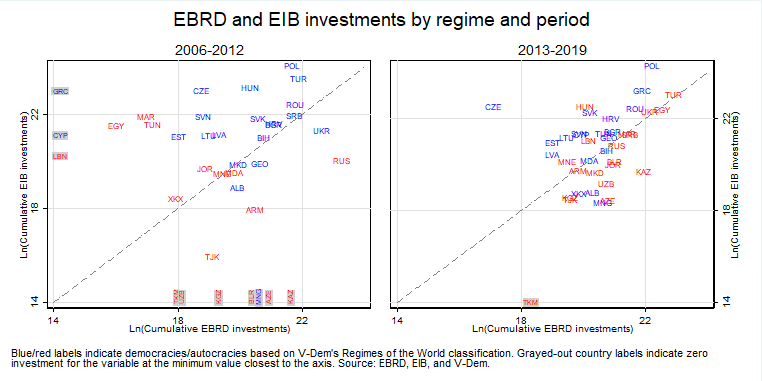

The EIB-weighted indices have also declined but to a significantly lower extent, which could be because the EIB universe is geographically very different than the EBRD’s. For this purpose, I restrict the sample to only countries where the EBRD has ever invested in and plot the natural logarithm of the cumulative EIB and EBRD investments for the periods 2006-2012 and 2013-2019 against each other. Points on the diagonal line would thus indicate that both institutions invest an equal amount in the country.

In both time periods, the EIB tends to invest larger sums in democracies than the EBRD. As for investments in autocracies in the earlier period, the EIB is more invested in the Middle East than the EBRD, whereas the latter has more activity in Russia and some Central Asian countries (where EIB investments were zero, as indicated by the gray labels on one side of the axis in the graphs). In the latter period, the EBRD has increased its investments in several democracies yet, and as shown before, even more so in autocracies where the EBRD branched out into especially the Middle East while also expanding operations in Kazakhstan and Uzbekistan. In the latter period EIB and EBRD have also become more co-invested, and are especially correlated in countries like Egypt, Turkey, etc. Nonetheless, even within the sample of countries that the EBRD has ever invested in, the EIB tends to be more active in democracies.

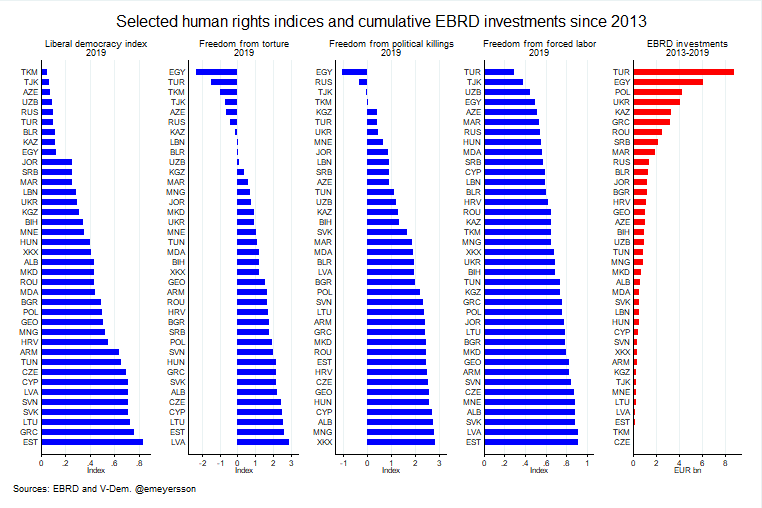

There is also worrying consequences for human rights abuses. V-Dem has three indices that are useful as measurement here: The Freedom from torture, Freedom from political killings, and Freedom from forced labor indices, which are hopefully rather self-explanatory. For all three indices the EBRD universe has fallen below the world median.

The reason for this deterioration, as well as that of Liberal Democracy, is perhaps unsurprising when countries like Azerbaijan, Egypt, Kazakhstan, Turkey and Uzbekistan have becoming a larger part of the EBRD universe. The below graph indicates a worrying association between some of the worst human rights abusers and some of the most attractive destinations investments for EBRD activity. The controversy around EBRD’s investments in autocratic countries is thus not simply a political one, it is also a human rights one.

The EBRD meets autocracy and crony capitalism

The rise in EBRD flows to autocratic countries is largely driven by four countries: Egypt, Turkey, and the Central Asian countries of Kazakhstan and Uzbekistan.

The EBRD turns a blind eye to repression in Egypt

The EBRD turning a blind eye to autocratic regimes’ excesses is clearly visible in Egypt. In August 2013, just after the country underwent a military coup bringing Sisi to power, Egyptian security forces killed just under a thousand demonstrators and wounded another four thousand in the Rabaa massacre. Yet despite all of this, within a year the EBRD had signed projects with a value of around €1.3bn. Two of these projects, totaling around 20% of this value, was with the Egyptian state.

And so, in one of the bloodier eras in recent Egyptian history, the EBRD found that this environment warranted Egypt to subsequently becoming its largest country of investment since 2018. And in that year, the boot of Sisi’s dictatorship was still being felt as Amnesty reported of the largest yet crackdown under his rule. As we saw from Figure 3, a significant share of investments in Egypt are with the state. Also, for some reason the EBRD classifies some investments as private even when they are with state-owned banks.

The EBRD summarizes its political assessment of Egypt’s commitment to democracy follows:

“Egypt is committed to and applying, albeit unevenly, the principles of multiparty democracy, pluralism and market economics in accordance with Article 1 of the Agreement establishing the Bank.”

The EBRD meets crony capitalism in Turkey

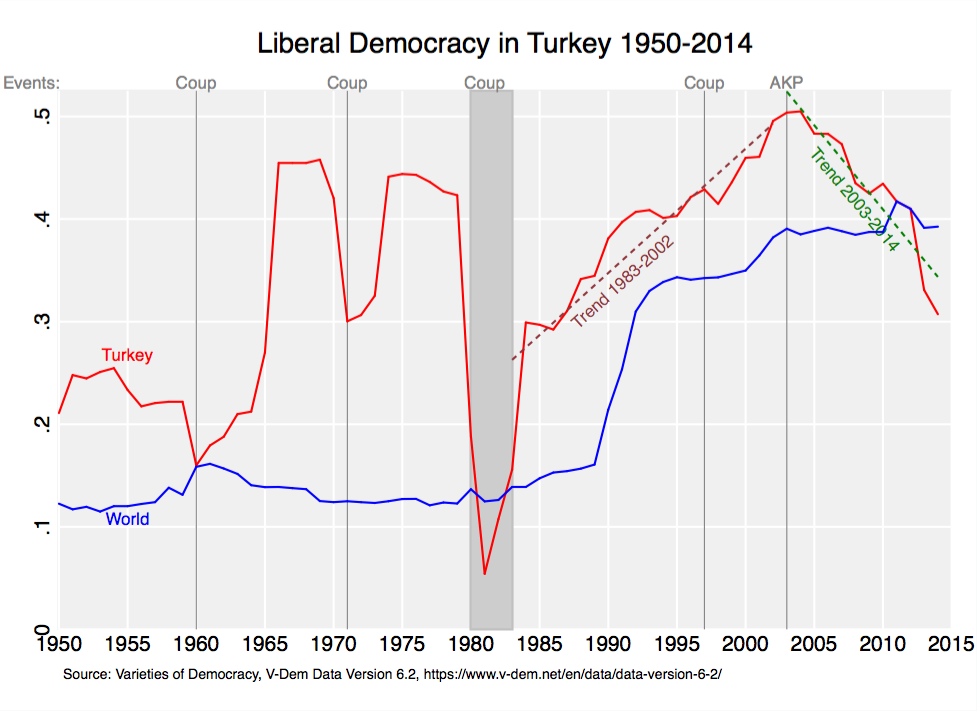

Since 2014 V-Dem has classified Turkey as an (electoral) autocracy according to its Regimes of the World (ROW) indicator. Freedom House has Turkey as “Not Free” in 2017. (Those who have followed my earlier work might come to the conclusion that Freedom House lagged realities somewhat.)

But EBRD doesn’t directly finance government projects here in any overwhelming extent. Instead, its focus is mostly on the private sector. The Bank seems to believe that financing the private sector in an autocracy insulates it from any negative spillovers. This year, the EBRD granted a long-term loan to a project to a private developer in a new municipal hospital. The company, Ronesans Healthcare, a subsidiary of Ronesans Holding which in turn is owned by Erman Ilıcak. Ilıcak is well-connected with the government, and is perhaps best known for building the presidential palace.

The links between the EBRD’s financing and the Turkish government’s connected businessmen can be found throughout the Bank’s activities in the country. Engaging with predominantly the private sector is thus far from a safety valve that it doesn’t become linked to the government’s authoritarianism. In a couple of cases, it reached foreign media. One example of this was when the EBRD found its investment in Borsa Istanbul connected to threats of US sanctions as the government decided to appoint the former Halkbank executive the post of CEO. This lead to the rushed sale of EBRD’s equity stake to the state-owned Turkey Wealth Fund (TWF), which later sold it on to the Qatar Investment Authority (QIA). By some accounts, TWF bought it from EBRD for roughly $122.5 million and selling it to QIA for $200 million. The difference, in the order of $77.5 million, could be interpreted as an advertent transfer of resources from the EBRD to the Turkish state.

The idea that EBRD investments in Turkey’s private sector somehow shield it from engaging with an autocratic government is ignorant of facts on the ground, as well as how political institutions in authoritarian countries work. Investing in the private sector in autocracies requires large resources in sourcing, due diligence etc to make sure that deals do not fall under the next of often extensive patronage networks operated by political elites.

Another incident involved the EBRD partnering up with SOCAR Turkiye, a subsidiary of Azerbaijan’s state oil company, in a business deal where the government appears to have intervened on the latter’s behalf in a legal dispute. The EBRD’s involvement with the Turkish and Azeri governments is also clear in the Southern Gas Corridor project, which is classified as a project in Azerbaijan but involves Turkey too. The financing extended (where the World Bank, the Asian Infrastructure Bank, and the European Investment Bank have also been involved) has been criticized by watchdogs for being “at odds with EU commitments on both human rights and climate action”.

The EBRD’s country strategy on Turkey’s commitment to Article 1 reads:

“Turkey’s commitment to, and application of, political principles as set out in Article 1 of the Agreement Establishing the Bank have, over the previous Country Strategy period, been under strain due to internal and external challenges, prompting relevant international organisations to express concerns.”

Senior management working with dictators in Central Asia, before and after EBRD employment

In Kazakhstan and Uzbekistan, the EBRD has invested roughly €10.2bn up until 2019, or three quarters of the region total, meaning the “EBRD in Central Asia” is essentially the “EBRD in Kazakhstan and Uzbekistan”. In the former, the EBRD has been active for more than a decade, whereas in the latter investments started only after 2017. The only real competition to these countries’ political institutions (as measured by V-Dem’s Liberal Democracy index) come from the likes of North Korea and Saudi Arabia. In 2018, the EBRD twitter account tweeted that it was the largest institutional investor in Central Asia, as well as accompanying infographic which included the following:

“Why You Should Invest With US – A Dynamic Region: The perceived risk of investing in Central Asia are relatively high. This has led to an increase in regional investment costs, a more expensive risk mitigation instruments often need to be built into investment revenue models. However, despite this perception of high risk, Central Asia is on of the most dynamic economic regions in the world.”

This sounded a lot like a marketing sales pitch. A marketing sales pitch for some of the more authoritarian regimes in the world. Such statements could leave the EBRD open to accusations that it has become a cheerleader for autocrats.

The renewal of operations with Uzbekistan came in 2017 after a visit by then EBRD Preisdent Suma Chakrabarti. The EBRD reportedly ended its engagement with Uzbekistan in 2007 after “bank’s ties with Uzbekistan soured over human rights concerns and a lack of political and economic reforms during late President Islam Karimov’s tenure.” RFE/RL quoted Chakrabarti as saying “I think there is a very strong commitment [to economic reform] from the top down.”

What is interesting here is the contributing factor of political institutions in the exit of EBRD in 2007, but no mention of any democratic improvement in its reentry. What is perhaps also somewhat concerning is that a few months after Chakrabrti left his position as President at EBRD, he became a personal adviser to the Uzbeki Preisdent. A few months before that he had also become the personal adviser to Kazakhstan’s president. Admittedly, the optics of this chain of events isn’t great.

With organizational survival at stake, needs must?

Survival risks and geopolitical events creates new frontiers

How does a bank who used to remain committed to multiparty democracy effectively cease to adhere to this? I don’t have a clear answer, but I have a hypothesis. And it involves another key component of the EBRD’s activities, its “additionality principle”, which states that “the Bank shall not undertake any financing, or provide any facilities, when the applicant is able to obtain sufficient financing or facilities elsewhere on terms and conditions that the Bank considers reasonable”. This is effectively meant as the EBRD should not compete with other organizations for financing projects.

An expected consequence of this is therefore that, within the original set of transition countries, as countries develop deeper financial markets of their own, the EBRD should cease activities in these regions. This has already occurred in the Czech Republic and could very well occur in more of these countries in the near- or medium term. Without the EBRD finding new pastures, its success would then ultimately result in its own dissolution. By the early 2010s, it was also clear that the geopolitical divergence between US and EU on one hand and Russia on the other meant the way was shut there as well. For any corporation that develops a sense of being, if not even a sense of self-importance, this could be challenging. But where to go to survive?

The Belt and Road Imitative was launched by China in 2013 and sent ripples through the balance of geopolitical power. But it also opened up significant business opportunities, as well as challenges. With China projecting more influence abroad, other powers like the EU were at risk of losing influence and possibly also access to natural resources. For some the BRI was the Great Game of the 21st century. But the EU didn’t have a development bank, it had the EIB and the EBRD – but which one would be most suitable to the task?

In addition, the Arab Spring in 2011 had overturned a number of autocratic stagnant regimes in the MENA region. A year or two later, new governments, some autocratic and some democratic, were looking to the outside world to aid in improving development outcomes.

For many academics and policymakers with some experience with transition, the Arab Spring and the MENA region looked like the natural next big project. But a key difference here was that, whereas the old transition countries came from being autocratic and planned economy systems, the MENA countries were also autocratic, but their economic systems were already to some extent market capitalist. For some of us, the primary instrument for change lay in the political institutions, and this what my former colleagues at SITE and myself wrote back in 2011:

One of the main insights from the transition experience is that both the ability to implement economic reforms and investor response to economic reforms implemented depends crucially on the political and institutional context. It is therefore not very meaningful to talk about the relative merits of particular economic reforms in isolation. Instead, more useful insights can be gained by addressing the role of political and institutional reforms in creating an environment in which investors can trust protection of property rights and contract enforcement, where political accountability and transparency contains corruption, state capture and cronyism, and economic reforms are politically feasible.

‘Modernization theory’ is the dictator’s best friend

It seems the EBRD had other plans. Instead it appears to have revamped a version of ‘modernization theory’ as a working ideology. This theory was popular during the Cold War, and in practice it was often used to support repressive dictators under the cover that they were pro-market and pro-reform. As Acemoglu, Johnson, Robinson, and Yared argues in their seminal 2008 paper “Income and Democracy”, “the central tenet of the modernization theory, that higher income per capita causes a country to be democratic”. The paper’s main finding is that, despite the statistical correlation, it is unlikely that this reflects a causality from income to democracy. Another paper by Guiliano, Mishra and Spilimbergo – published the same year as the EBRD report – but widely read long before that – has also shown that whereas democracy tends to predict economic reforms, the opposite does not seem to hold.

In its 2013 Transition report, the EBRD came out hard in favor of the modernization theory stating

“support for modernisation theory – the notion that economic development over time leads to democracy, albeit with some exceptions – has received strong empirical support in recent studies that cover long time series and control for several factors.”

EBRD Transition Report 2013, page 34.

The policy implications of this came right up front in the executive summary:

In order to support countries in their long-term transition to democracy, it therefore makes sense to encourage policies and institutions that underpin economic growth, foster market reforms, and assist countries that are rich in natural resources as they seek to diversify their economic base.

EBRD Transition Report 2013, page 5

A casual reader might get the impression that the EBRD had thus found academic research support for engaging with autocracies, especially resource-rich ones like Kazakhstan and Uzbekistan. At the time of the writing of this report, I was working on my own paper on this topic and was heavily invested in the literature. A deeper review of the econometrics of the EBRD report is outside of the scope here, but my own impression was that these conclusions were based on econometric analysis that were not state of the art at the time (I would urge the reader to read chapter 2 of the report, and consider whether the use of estimator, sample size, coefficient size, level of statistical significance, and construction of dependent variables in eg. table 2.2 correspond to the state of the art). But perhaps more concerning, neither the AJRY or the GMS paper were referenced or discussed. These were critical to the topic of discussion and had conclusions that ran counter to those in the EBRD report – and perhaps also, EBRD corporate strategy. As a former journal editor and referee, I would have objected to the presentation of the results if this had been an academic paper, as I would the the conversion of the empirical results into what I would consider to be overly strong policy implications.

This of course doesn’t necessarily mean the debate on the relation between income and democracy is completely settled. Later research has shown that there exists heterogeneity in the correlation between income and democracy, and – in political science – there is an argument that very large increases in income per capita, over certain time periods, predicts democratization. None of these, however, would necessarily lend strong support to an EBRD drive into autocratic resource-rich countries.

Last year, the EBRD’s exclusive interpretation of institutions returned, but this time in a less internally consistent manner. The foreword and executive summary noted the importance of “voice” and “accountability” in its relatively broad definition of institutions, yet when it came to measuring institutions the report specifically excluded one indicator aptly named “voice & accountability”, which included a number of subindicators relevant for the measuring of economic institutions. The analysis ended up putting some countries, especially Turkey, in better light than it arguably deserved. (The same report also included a curious incident of a text box removed from the online version which indicated adverse socioeconomic effects of Ottoman rule in Eastern Europe.)

The implications of the EBRD’s official research output seems to yield roughly the same conclusions as that of Cold War modernization theorists: Aiding and abetting autocratic – albeit “market-friendly” – leaders is advisable under the presumption that these economic reforms will lead to higher economic growth, and later on, sets the conditions for democracy. The belief in modernization theory, with democracy serving as a “crowning institution” means financing autocracy goes from being a moral problem to potentially a moral necessity.

The release of 2013 report and its conclusions coincided with the EBRD’s controversial expansion into Egypt and subsequently Central Asia. As such, in its controversial decision to partner up with a ruthless dictator who just usurped power through a military coup, the EBRD could to some extent claim to have research on its side. Yet the arguments for doing so seemed to resonate with similar ones from around the world in 1965, 1973, and 1980.

The sustainability of EBRD’s investments in autocracies

Most of the EBRD’s investments with autocratic governments fall under the category “Sustainable infrastructure” which includes Energy, Municipal & Environmental infrastructure, and Transport projects according to its classification scheme. A significant part of this falls under the Sustainable Energy Initiative (SEI) which as “the aim of scaling up sustainable energy investments in the Bank’s region, improving the business environment for sustainable investments and removing key barriers to market development.” The below graph shows EBRD investments by sector and regime type for the time periods 2006-2012 and 2013-2019 respectively. This illustrates the extent to which the EBRD’s investments in its sustainability projects (the bottom bars in the graph) has increased in autocracies after 2013.

This suggests that even if the EBRD’s sustainability investments may be green environmentally, they are still quite “brown” politically. But why are the EBRD’s sustainable investments so overwhelmingly in autocracies? Could it be that it’s easier to defend financing autocratic governments if you can claim to make the planet greener or more sustainable in the process?

Overall, it seems that the EBRD has found a way to convince itself of the benefits of financing autocratic countries and governments. Its past research, in leaning on a controversial development view with origins in the Cold War, claims this could ultimately lead to increased prosperity and eventually democracy. Structuring these investments as green or sustainable projects means it’s in line with broader EU strategies of shifting towards a greener economy. Meanwhile, the bank faces less of a risk of extinction from its additionality principle and looks to take pole position as a candidate for the EU’s future development bank as the it faces off geopolitically with the US and China.

The EBRD’s version of transition risks losing its soul

The problem with the EBRD’s apparent crossbreeding between transition and modernization theory is that it discounts the importance that political institutions play in promoting development. Any academic or policymaker working with development-related issues today would have to struggle hard to avoid this. This does not mean you have to believe democracy causes economic development, it merely means being critical of the supposition that a correlation between the two should mean financing autocratic regimes is advisable. Yet at the EBRD, political institutions appear to have become subordinate to other factors, characterizing no only their official research output but also – and more importantly – their actions.

The EBRD cannot realistically push for regime change in its member countries, but it can realize that without a real commitment (rather than a cosmetic commitment that reaches the threshold of the EBRD’s ludicrous process of determining whether Article 1 is satisfied) to democracy, development will be much more difficult, and the EBRD’s actions will be morally much more questionable. At the time of EBRD’s conception, Article 1 may have been seen as more of a moral or political requirement as much as an instrumental one. After all, in 1991 the empirical political economics literature had little meaningful to say about the effect of democracy on economic development. Today, that situation is quite different. Recent work shows that the the degree to which democracy statistically predicts economic growth is so robust that economists way more famous than I have interpreted this relationship as causal. Others have also shown that democracy seems to drive economic reforms, whereas the opposite does not seem to hold.

There’s nothing wrong with EBRD’s research output providing a minority report, but it in drawing strong and contrarian policy implications from it, it further coincides with a business drive towards autocratic regimes that not only violates its own stated articles, but also seems careless and immoral, if not even self-serving. Geopolitical as well as organizational needs may be explanatory factors in this shift.

The main destination of this post, however, isn’t the research section of the EBRD. Despite some of my comments about the official reports, the EBRD has throughout the years consistently produced excellent research output in academic publications and its working papers. Instead, this is an issue for management and the bank’s shareholders. The Bank has clearly moved away from its original statues. Either it changes course or it changes the statues. If the real goal is to go from a regional development bank that invests in democracies to a development bank that invests with geopolitical interests in mind, this should become more clearly stated. The EU and the EBRD wouldn’t be the first institutions to realize that interests trump values. We don’t observe the real reasons for the EBRD’s actions because they are poorly, if at all, explained. There is practical debate to be had over the costs and benefits of the EU and its institutions moving to new frontiers in development banking, and the EBRD plays an important role in this.

As it stands, the EBRD and its – recently turned more authoritarian – brand of transition risks losing its soul and with it many of the lessons of the transition process in central and eastern Europe. As authoritarian tendencies can once again be seen throughout the formerly Eastern bloc, one can’t but help wonder if things might have been different if international institutions had focused as much on political – as they did on economic – institutions. After all, if liberal democratic change struggles to gain a foothold in many parts of Europe even after market capitalism is implemented, why should we expect this to occur at all in countries like Egypt, Turkey or Uzbekistan? And if it doesn’t happen, what is the point of pursing development projects with corrupt and autocratic regimes if at some point they don’t develop inclusive institutions? Who benefits from that?

Besides the EBRD, that is.

{kind=link}

{kind=link}

{kind=link}